South Korean stocks are expected to look for direction this week as they absorb heightened volatility. Semiconductors have led gains in the KOSPI, but fatigue has also grown after a short-term surge. Market attention is on whether buying can shift from semiconductors to other sectors.

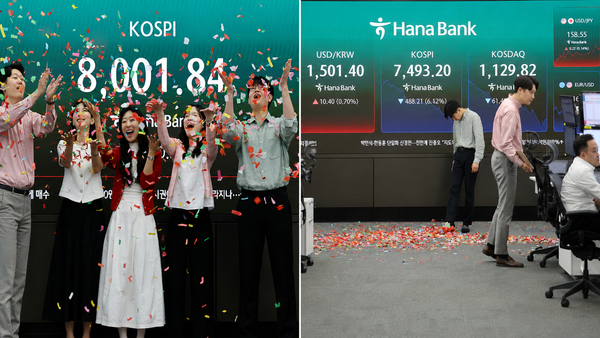

The KOSPI broke above the 8,000 mark for the first time ever in intraday trading on May 15, but later plunged. The index ended at 7,493.18, down 488.23 points, or 6.12 percent, from the previous session. The KOSDAQ also finished down 5.14 percent at 1,129.82.

A flood of intraday selling triggered a sell-side circuit breaker. With stock prices having risen too fast in a short period, rising interest rates, a sharp jump in the exchange rate and foreign selling combined to quickly dampen investor sentiment.

The biggest backdrop to this adjustment is the concentration in semiconductors. Since the start of May, the KOSPI has jumped 1,380 points, or 20.1 percent, in just 8 sessions, approaching 8,000. The semiconductor sector accounted for 85.3 percent of that rise.

Expectations for results at Samsung Electronics and SK Hynix pushed the index higher. But as buying became overly concentrated in a single sector, the burden of profit-taking also grew.

Interest rates and the exchange rate also weighed on the market. The U.S. 10-year Treasury yield topped 4.5 percent, and the 3-year and 10-year South Korean government bond yields rose to around 3.75 percent and 4.2 percent, respectively. The exchange rate rose above 1,500 won intraday for the first time in about a month.

If interest rates and the exchange rate rise at the same time, the burden of investing in South Korean stocks can increase for foreign investors. Foreigners were net sellers for 7 consecutive sessions, with cumulative net selling expanding to around 32 trillion won.

Still, the industry sees the latest plunge as closer to cooling overheating than breaking the upward trend itself. The KOSPI's 12-month forward price-to-earnings ratio has recently recovered to around 8, but it is still low compared with past averages.

That means that although the index has risen sharply, corporate earnings forecasts have also increased, making it hard to say stocks have become unconditionally expensive.

The key this week is which sectors move after semiconductors. As the first-quarter earnings season nears its end, the pace of upward revisions to semiconductor earnings forecasts could slow somewhat. In that case, buying could shift to sectors that rose less in the recent rally or where share prices reflect earnings less.

The industry sees chemicals, energy, healthcare, software, banks, IT appliances, brokerages, cosmetics and apparel, and consumer staples as candidates for sector rotation. These sectors are seen as having had relatively weaker recent share price gains or as not yet fully reflecting expectations for earnings improvement.

Economic data are also important. On May 18, China is set to release real-economy indicators including retail sales, industrial output and fixed-asset investment. If signals emerge that China's economy is improving, that could be positive for chemicals, energy, cosmetics and consumer staples. A pickup in Chinese consumption and production could also lift expectations for exports and results at South Korean companies.

On May 21, the Philadelphia Fed manufacturing index and S&P Global manufacturing and services purchasing managers' indices are due. If it is confirmed that the U.S. economy is solid, export and materials stocks could gain support. If the data are weak or pressure for higher rates grows, growth stocks and highly valued sectors could be shaken again.

Geopolitical variables also remain. It is positive that the two countries showed a conciliatory stance at a U.S.-China summit, but uncertainty related to Iran has not yet been resolved.

West Texas Intermediate crude futures are holding above $103 a barrel. If oil prices stay high, the inflation burden would grow and that would lower expectations for rate cuts, weighing on stocks.

In the short term, some also cite the possibility that a correction or sideways trend could continue from mid-May to mid-June. They cite the need for time for the market to digest the inflation burden, rising interest rates, a weaker won and events scheduled in June. After earnings announcements end and before the next earnings outlook emerges, drivers that push the market higher could temporarily weaken.

Over the medium to long term, the possibility of the KOSPI reaching 10,000 has also been raised. The KOSPI's estimated net profit in 2026 is forecast at 689 trillion won, rising to as much as 853 trillion won in 2027.

Applying the average price-to-earnings ratio since 2010 also yields calculations showing the upper end of the KOSPI could exceed 10,000. But that requires the premise that semiconductor earnings forecasts continue to hold.

Ultimately, the key for the market this week is how much other sectors can support the index while semiconductors take a breather. If Chinese and U.S. economic indicators are favorable and oil prices, interest rates and the exchange rate stabilize, sector rotation could spread to materials, consumer goods and growth stocks.

If high oil prices and high interest rates persist and exchange-rate instability continues, the KOSPI could face an additional correction after breaking above 8,000.

Lee Kyung-min (이경민), a researcher at Daishin Securities, said, "Since the start of May, the KOSPI surged 1,380 points, or 20.1 percent, in just 8 sessions, moving close to 8,000, and semiconductors accounted for 85.3 percent of the KOSPI's sharp rise." He said, "With fatigue accumulating from gains in the KOSPI and the semiconductor sector and the burden of overheating growing, it is time to prepare for non-semiconductor shares rising alongside or showing relative strength after the early-month surge in semiconductors."