A Cornell University student in the United States has drawn attention after releasing an interactive calculator showing how retirement assets could change if Social Security taxes, or payroll taxes, were invested in Strategy's STRC preferred shares.

On March 31 local time, blockchain media outlet BeInCrypto introduced the tool presented by bitcoin advocate Ella Hough (엘라 허프).

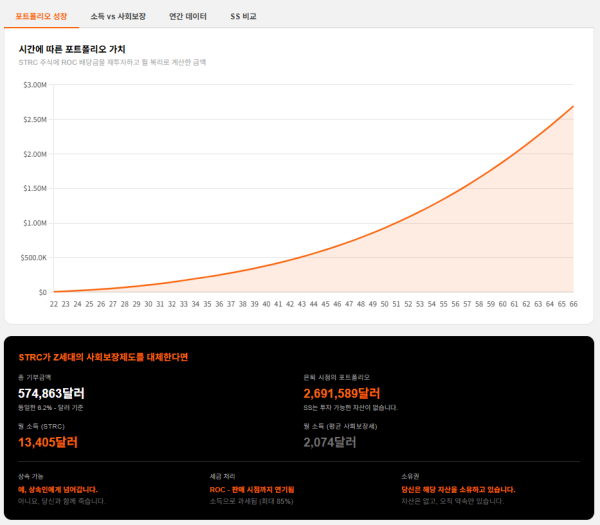

Hough's model assumes a 22-year-old worker earns an annual salary of $100,000. It uses a scenario in which the worker redirects a 6.2 percent payroll tax contribution into Strategy's STRC. STRC currently pays an annualised dividend of 11.5 percent and is trading on Nasdaq near its $100 par value. It also said STRC's volatility over the past 30 days was lower than stocks included in the S&P 500 and major asset classes.

The calculator applies a condition that dividends are reinvested monthly. It assumes returns decline linearly as retirement approaches, reaching 6 percent at age 67. Under that scenario, the portfolio value at age 67 becomes $2.69 million, and monthly dividend income is estimated at $13,405.

As a comparison, it presented an average monthly Social Security pension benefit of $2,074. A 2025 SSA trust fund report forecast the fund would be depleted in 2034, and predicted that after that it would be able to pay only 81 percent of scheduled benefits.

It also said the risks tied to the assumptions need to be considered. STRC's dividend is not guaranteed and Strategy's board can adjust it monthly, it said, adding that the risks are large. STRC preferred shares are also not directly collateralised by Strategy's bitcoin holdings of 762,099 BTC.

Hough posed the question: "Weekend thought experiment: What if Social Security for Gen Z could look a little more like STRC?" Comments raised issues including that real returns could be eroded by 45 years of inflation, the possibility of dividend cuts, and that shifting payroll taxes would require legislation by Congress. Some said direct investment in bitcoin or in Strategy common stock (MSTR) could be better than dividend products, among other views.

The tool is seen as an example that puts into numbers Gen Z anxiety about pensions and interest in alternative investments. It also drew an assessment that an "opt-out" plan to redirect payroll taxes into a specific financial product would require institutional change and political agreement, leaving it still far from being realised. It concluded that the discussion is less about STRC's investment appeal than it is a scene showing how much distrust of the existing Social Security system has grown among younger generations.

Weekend thought experiment: What if Social Security for Gen Z could look a little more like $STRC? TL; DR: Today, if a 22 y/o could redirect their 6.2% payroll tax into $STRC, at age 67, they could retire with ~$13,000/mo vs. ~$2,000/mo. Try it out yourself below! pic.twitter.com/F9OEctGJkY