The Korea Capital Market Institute (KCMI) forecast the KOSPI could rise to 5,500 to 6,000 this year as improving corporate earnings coincide with results from the value-up programme.

KCMI on Jan. 27 assessed the domestic stock market and held in-depth discussions on tasks for the securities industry in 2026 at its "2026 capital market outlook and key issues" seminar at the Financial Investment Center in Yeouido, Seoul.

KOSPI expected to see an IT-led profit cycle in 2026

Kang So-hyun (강소현), head of KCMI’s capital markets office, assessed 2025 as a year in which the stock market delivered the most notable performance among major global markets. In 2025, the KOSPI rose 75.6 percent from a year earlier and the Kosdaq gained 36.5 percent, setting new record highs.

Kang analysed that in the first half of 2025, the government’s corporate value-up programme and expectations of governance improvements eased the "Korea discount" and led the rally. She said in the second half, expectations of earnings improvement driven by a recovery in the semiconductor cycle took over.

In particular, the market capitalisation share of the information technology and semiconductor sectors exceeded 45 percent, and a structural feature became clear in which reliance on specific large-cap stocks such as Samsung Electronics and SK Hynix surpassed 35 percent.

On the outlook for 2026, she said that, based on analyst forecasts, listed companies’ operating profit in 2026 is on an upward trend. She said the operating profit growth rate for the IT sector, in particular, is expected to widen sharply from a year earlier. She forecast that if improving earnings provide support, reaching 5,500 to 6,000 on the KOSPI is sufficiently possible through valuation normalisation.

But she pointed to polarisation as a continuing challenge. Kang said that even during the rally in the second half of 2025, among mid- and lower-market-cap stocks, declining stocks outnumbered rising ones by 2 to 3 times. She said that the intensifying concentration in a small number of large-cap stocks is a risk factor because momentum is not spreading across the broader market.

Securities industry sees joint growth in brokerage and IB; AI shift is key to survival

Lee Seok-hoon (이석훈), head of KCMI’s financial industry office, forecast that profitability in the securities industry in 2026 will expand on the back of balanced growth in brokerage and investment banking (IB).

Lee said that profitability improvement is clear, with the securities industry’s equity capital rising 9.8 trillion won in 2025 and return on equity (ROE) at 8.6 percent. He analysed that in 2026, brokerage fee income will increase as domestic and overseas stock trading grows, and IB performance will also be strong as functions supplying risk capital, such as corporate credit provision and issuance of promissory notes, are strengthened.

He also highlighted changes in the retirement pension market. Lee said the introduction of default options for retirement pensions is accelerating the shift of funds to performance-linked products. He said this will become a new source of revenue for securities firms’ wealth management (WM) divisions.

On real estate project financing (PF) risk, he said expansion in the size of securities firms will be limited due to an overhaul of risk weights for the net capital ratio (NCR) and stronger provisioning requirements. He assessed that soundness would instead improve through strengthened qualitative management.

He cited an "artificial intelligence (AI) shift" as a key topic for the securities industry. Lee said overseas securities firms are already using generative AI across operations such as research and compliance to boost efficiency. He stressed that domestic securities firms must go beyond simply introducing chatbots and stake their survival on building companywide AI governance and developing customised services.

Overseas stock concentration needs to be addressed with futures-based FX-hedged ETFs

Kim Doo-nam (김두남), a vice president at Samsung Asset Management, who attended as a panellist, said that in 2025 net buying of overseas ETFs listed in South Korea, as well as retail investors’ direct investment in overseas stocks, reached 17 trillion won. He pointed out that if spot gold ETFs are included, foreign-currency outflows through ETFs alone exceed 23 trillion won.

As a solution, Kim proposed activating "futures-based FX-hedged ETFs." He said futures-based ETFs hold the principal in won, excluding margin, reducing exchange-rate volatility and contributing to stabilising supply and demand in the foreign exchange market. He argued that institutional improvement is urgent because investment in futures-based ETFs is currently not allowed in retirement pensions.

Choi Ji-wook (최지욱), chief economist at Korea Investment & Securities, said expanding overseas investment by the National Pension Service and retail investors’ concentration in overseas stocks are increasing downward rigidity in the won-dollar exchange rate. He added that the government’s value-up programme must lead to a real rise in the attractiveness of the domestic stock market to prevent funds from flowing overseas.

Financial Services Commission to shift real estate-concentrated funds to risk capital

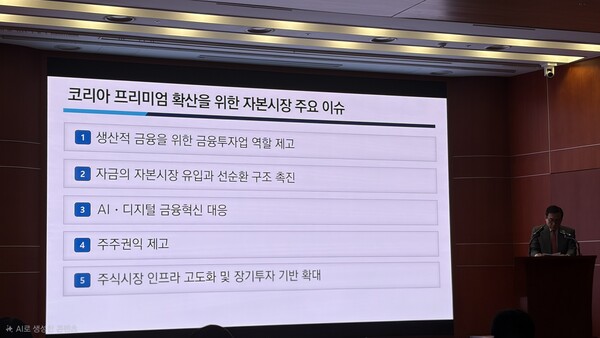

Choi Chi-yeon (최치연), head of the Asset Management Division at the Financial Services Commission, said policy capabilities in 2026 will be focused on a major shift of funds concentrated in real estate to risk capital, such as venture and innovative companies. He said this would realise a "Korea premium" and dramatically increase the attractiveness of South Korea’s capital market.

He cited specific measures including institutionalising securities firms’ obligations to supply risk capital, introducing business development companies (BDCs), and overhauling regulation on private equity funds (PEFs).

Choi said that through new licences for large securities firms and making risk-capital supply obligations mandatory, an additional 27 trillion won in risk capital is expected to be supplied by the end of 2028 compared with the end of 2025.

He also added that incentives for small and medium enterprise-focused securities firms will be improved to strengthen their capabilities to support small and venture companies.