Attention is focused on whether the KOSPI will extend its unrelenting run into March. The benchmark ended last year around the 4,200 level, then broke above 5,000 at the end of January. It moved past 5,500 and 5,800 in February and topped 6,000 before the month ended. Average daily turnover exceeded 30 trillion won for the first time. This month, analysts see unavoidable negative short-term effects after the United States and Israel launched large-scale attacks on Iran.

According to the Korea Exchange on March 3, average daily trading value in the KOSPI last month hit a record 32.234 trillion won. That was up 19 percent, or 5.178 trillion won, from January's 27.056 trillion won.

The move is seen as the result of a daily rally fueled by a boost from U.S. technology stocks and expectations that a third revision to the Commercial Act would pass.

Turnover was concentrated in large semiconductor stocks. Average daily trading value in Samsung Electronics, SK Hynix and Samsung Electronics preferred shares totaled 10.502 trillion won last month, accounting for 33 percent of total KOSPI turnover.

Trading turnover was also brisk, with the KOSPI market share turnover rate at 28.0 percent last month, the highest in 3 years and 10 months since April 2022.

With the KOSPI surging in a short period, the burden of a peak has also grown. Geopolitical tensions in the Middle East and uncertainty over the Trump administration's tariff policies are adding external variables. Analysts see profit-taking emerging early this month.

Brokerage firms say concerns are growing over a closure of the Strait of Hormuz and a spike in oil prices after the death of Iran's Supreme Leader Khamenei, but they see a low chance of the situation heading to an extreme.

Choi Jin-young (최진영), a researcher at Daishin Securities, analysed that the possibility of a prolonged conflict is low due to a power vacuum in Iran and a neutrality declaration by its ally Lebanon. He said it would be difficult for Iran to push through a full blockade because the Strait of Hormuz is its key source of war funding.

Another factor expected to calm oil price instability is that OPEC+, a consultative body of major oil-producing countries, is considering resuming output increases from April.

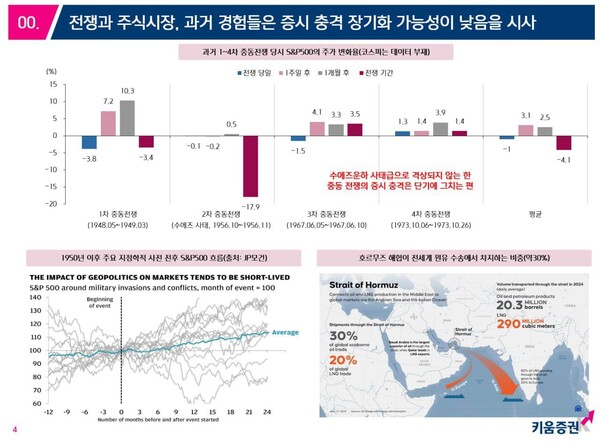

Based on past cases, the prevailing view is that any shock to stock markets will also be temporary.

Han Ji-young (한지영), a researcher at Kiwoom Securities, said the S&P 500 fell 1.0 percent immediately after the war and rose 3.1 percent a week later during the first to fourth Middle East wars, recouping the earlier drop. He said an increase in short-term price volatility is unavoidable, but the negative impact on direction will be limited unless the situation escalates into an all-out war.

This month, the KOSPI is expected to absorb a short-term adjustment tied to the Middle East situation and then look for direction depending on corporate earnings and key macroeconomic schedules.

Lee Kyung-min (이경민), a researcher at Daishin Securities, said the KOSPI is rising mainly on upward revisions to profit forecasts in semiconductors, making it different from past liquidity-driven markets. He said the trend of record-high moves itself is unlikely to reverse.

Still, with full-fledged first-quarter earnings releases approaching, the market's upward momentum could slow somewhat.

Lee said profit forecast upgrades could stall until late-March shareholder meetings and the pre-earnings season for the first quarter. He also said major uncertainty factors, such as whether a hearing schedule will be confirmed for Kevin Warsh as the next Federal Reserve chair, are expected to be key variables that increase market volatility this month.