Value-added telecommunications services continue to grow. Sales from value-added telecommunications services topped 500 trillion won in 2024, rising 15.3 percent from a year earlier.

The Ministry of Science and ICT on Tuesday released the results of its 2025 survey on the value-added telecommunications business. The survey aims to assess the value-added telecommunications market and use the findings for related policy. This year’s survey also added a study of user behaviour for major digital platform services and a survey of bundled sales of digital platform services.

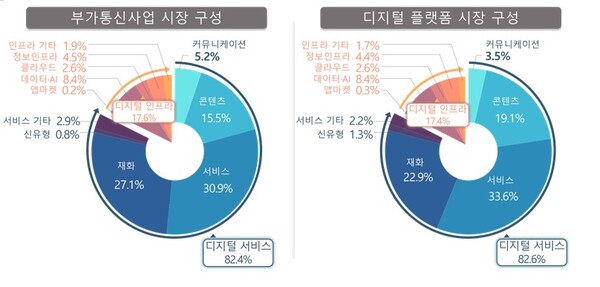

The types of services provided in 2024 by 1,451 value-added telecommunications operators that responded to the survey, based on their flagship services, were led by service provision such as food delivery and travel and accommodation reservations at 30.9 percent. Goods transactions such as e-commerce followed at 27.1 percent. Content provision such as search and games was 15.5 percent. The survey found 59 percent provided two or more types of value-added telecommunications services.

Among the respondents, 765 companies, or 52.7 percent, were digital platform operators. The service types offered by digital platform operators were services at 33.6 percent, goods at 22.9 percent and content at 19.1 percent. The survey found 68.2 percent provided two or more service types.

Value-added telecommunications service revenue in 2024 was estimated at 502.9 trillion won. Of that, digital platform service revenue was 161.5 trillion won, accounting for 32.1 percent of value-added telecommunications revenue. From a year earlier, value-added telecommunications service revenue rose 15.3 percent and digital platform service revenue increased 5.4 percent.

In a survey on the use of digital technology by value-added telecommunications operators, 62.2 percent of responding operators used at least one new digital technology. The figure was higher at 75.2 percent for digital platform operators. Both groups used technologies in the order of artificial intelligence, big data and cybersecurity, while digital platform operators had higher usage rates for every technology than value-added telecommunications operators.

Difficulties cited by value-added telecommunications operators in pursuing business included securing specialised staff for the latest technologies, a lack of government support for industrial promotion and the burden of infrastructure costs. The survey found they also had difficulties with marketing and distribution for overseas expansion, obtaining information on localisation and legal systems, and securing support staff.

The ministry also conducted a user survey of 2,500 adults aged 19 to 69 living across South Korea’s 17 provinces and major cities to identify usage patterns of major digital platform services.

By platform type, usage experience from October to December 2025 was highest for search at 98.7 percent, messenger services at 98.5 percent, place and map services at 96.8 percent, e-commerce at 95.6 percent and video-sharing at 92.7 percent. Daily usage frequency was led by messenger services at 91.3 percent, search at 85.8 percent and video-sharing at 69.5 percent.

Over the past three months, the share of users who used two or more platforms in parallel was highest for e-commerce at 83.9 percent, social media at 79.9 percent and search portals at 76.9 percent. By contrast, secondhand trading at 25.9 percent and app markets at 24.9 percent were relatively low. In particular, e-commerce and social media users used an average of three or more platforms, confirming more active multi-homing than in other categories.

The survey also examined the status of bundled platform sales amid the spread of subscription services. Bundled platform sales refer to a model in which platform companies provide multiple services as a package in exchange for subscription fees. It offers better value than individual subscriptions but can also raise concerns about limiting competition in adjacent markets or locking in users.

In the survey of 2,500 adults, 1,347 respondents, or 53.9 percent, said they had experience subscribing to an over-the-top streaming service membership. Among membership subscribers, SKT, KT, LG Uplus and Tving+Wavve were most common, in that order. The rankings for OTT subscriptions surveyed separately and the rankings of OTT services used under telecom-company OTT memberships mostly matched, indicating telecom-company OTT bundling does not have a large impact on the OTT market.

Respondents with experience subscribing to an e-commerce membership totalled 1,897, or 75.9 percent. The main memberships used were Coupang Wow, Naver Plus, Shinsegae Universe and U+ Pass, in that order. Looking at reasons for subscribing and switching, the survey found Naver competes on price rationality and linked services, while Coupang competes on fast and low-cost delivery.