Ahead of its planned launch in May, market expectations and concerns are intersecting over the public-participation National Growth Fund. It will collect money from ordinary citizens to invest in strategic advanced industries and offers sweeping tax benefits. But it is also drawing attention for liquidity burdens from long-term investment and a debate over effectiveness.

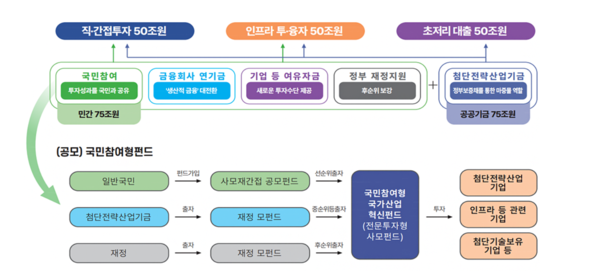

According to the National Assembly and the financial sector on the 23rd, the public-participation fund is a retail-focused product prepared as part of the National Growth Fund, which is being formed at a total scale of 150 trillion won.

It is structured as a separate 3 trillion won tranche over 5 years, or 600 billion won a year, carved out of the National Growth Fund. The National Growth Fund is a large policy fund led by the government and the financial sector to support the national advanced-industry ecosystem. The retail tranche is designed to let ordinary citizens invest directly and share returns.

The key draws of the retail fund are recently detailed tax benefits and a loss-protection mechanism.

Subscribers can receive income deductions of 40 percent on investments up to 30 million won, 20 percent on 30 million won to 50 million won, and 10 percent on 50 million won to 70 million won. Tax benefits can total up to 18 million won.

The investment cap per person is up to 200 million won. A separate tax rate of 9 percent also applies to dividend income.

The Financial Services Commission on April 10 released criteria for selecting sub-fund managers and announced that more than 60 percent of committed capital must be invested in 12 strategic advanced industries, including AI, semiconductors and bio.

At least 30 percent will be invested as new money in unlisted firms or KOSDAQ-listed companies that went public under a technology special listing scheme, playing a role as venture capital. It also set a policy to prioritise allocation of at least 20 percent of the fund's sales amount to low-income people to provide opportunities to build assets.

But behind the benefits, there are many risks and issues investors must bear. The biggest obstacle is a closed-end structure that locks up money for 5 years after subscription.

Even if investors need cash mid-way, redemption is in principle close to impossible. Investors must also keep their holdings for at least 3 years to secure the tax benefits, creating a very large burden on retail investors in terms of liquidity.

This almost matches a drawback that had been pointed out in the "Youth Leap Account", a youth asset-building support programme under the previous Yoon Suk Yeol government. The early termination rate for the Youth Leap Account was tallied at 20.2 percent.

The long-term investment requirement is also spreading into a controversy over tax cuts for the wealthy. While the policy prioritises 20 percent of allocations for low-income people, receiving the full maximum income-deduction benefit of 18 million won requires parking a lump sum of 70 million won for 5 years.

Because it is a condition that low-income and middle-class people are realistically unlikely to shoulder readily, critics say it could end up as a tax-saving channel only for high-net-worth investors with ample spare cash.

Concerns about mis-selling are another task to address. To encourage private participation, the government will act as a subordinated investor and set up a buffer mechanism to absorb up to 20 percent of fund losses first.

But this means that if total losses exceed 20 percent, individual subscribers can also lose principal. If sales channels exaggerate the fund as principal-guaranteed or a safe asset, it could later lead to large-scale consumer harm.

Uncertain returns and the method of paying dividends also reduce its investment appeal. Because it is a government-led fund with a clear policy purpose, a prevailing view is that it will be difficult to deliver high returns on par with private equity funds in the broader market.

Precedents in which major policy funds launched in the past delivered results below market expectations are also heightening investor doubts. No clear guideline has yet been presented on how dividends, a key part of returns, will be paid and at what interval.

Financial authorities say they will focus on strengthening management capabilities to ensure the fund settles successfully despite market concerns.

An FSC official said, "We will complete the selection of managers by mid-May, go through preparation steps including filing a securities registration statement, and then officially launch the product in May." The official added, "We will seek to improve the public's actual returns, including by providing additional incentives to managers with strong performance."