South Korean stocks face a week packed with major events, including U.S. inflation data, a Bank of Korea monetary policy meeting, MSCI rebalancing and the launch of single-stock leveraged and inverse exchange-traded funds (ETFs). The market is expected to keep testing whether the KOSPI can settle around 8,000 and whether rotation into Kosdaq growth stocks can be sustained.

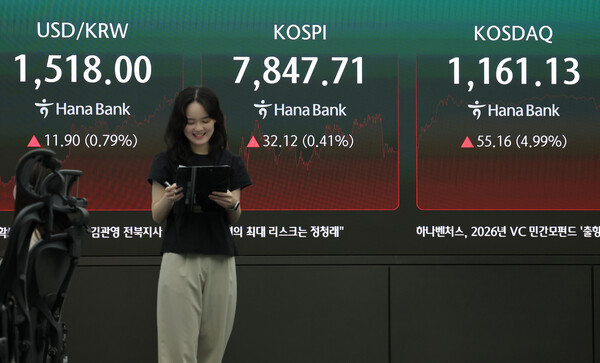

On May 22, foreign investors net bought about 600 billion won on the Kosdaq, while institutions net bought 290 billion won. On the same day, the KOSPI rose 0.41 percent to 7,847.71 and the Kosdaq jumped 4.99 percent. South Korean stocks ended last week with strength in the Kosdaq.

Expectations have risen that funds could flow into advanced industries such as pharmaceuticals and biotech, robotics, and aerospace after the launch of the National Growth Fund. The Kosdaq triggered a buy-side circuit breaker for two consecutive sessions.

Some in the market also say the KOSPI has entered a period of "unprecedented volatility," swinging between sharp gains and declines. The KOSPI rose more than 606 points on May 21 alone, marking the biggest one-day point gain on record.

The first variable this week is economic data. Due on May 25 are the U.S. April Chicago Fed National Activity Index. On May 26, the U.S. house price index and consumer confidence index are scheduled. On May 27, South Korea's March population trends and a May business survey are due, along with the U.S. Richmond Fed manufacturing index.

On May 28, South Korea's first-quarter household trends survey, the euro zone's May economic sentiment index, the U.S. April personal consumption expenditures (PCE) price index and new home sales will be released. On May 29, South Korea's April industrial activity trends and China's manufacturing and services purchasing managers' indices (PMI) are due.

The U.S. PCE price index on May 28 is a key indicator that can influence the rate outlook. Markets have recently seen oil prices, interest rates and the currency rise at the same time. Some in the industry say it is difficult to conclude that the stock market's upward trend has been immediately broken by rate burdens alone because corporate earnings forecasts remain strong.

The Bank of Korea meeting is also important. At the May 28 meeting, attention will be on whether the central bank keeps its policy rate unchanged and on its messages about inflation, the currency and the economy.

If the Bank of Korea sends a hawkish signal as the won remains weak and oil prices stay high, volatility in growth stocks and the Kosdaq could increase. If rate burdens ease, additional buying could emerge in overlooked growth stocks such as pharmaceuticals and biotech and internet shares that have recently been strong.

On flows, the launch on May 27 of two-times single-stock products tied to Samsung Electronics and SK Hynix is another variable. Sixteen single-stock leveraged and inverse products using Samsung Electronics and SK Hynix as underlying assets are set to list on the domestic market.

Because the underlying assets have large market capitalisations and heavy trading, the initial impact on direction may be limited. Still, if product size grows and volatility in the underlying assets increases, volatility from rebalancing near the close could rise. Investors also need to be mindful of the negative compounding effect that can reduce principal as prices rise and fall, a characteristic of leveraged products.

These products are likely to draw investor interest. Two-times leveraged products tied to Samsung Electronics and SK Hynix listed in Hong Kong have already been popular with South Korean investors. Some in the industry believe some funds that flowed overseas could return home as domestic listings reduce issues such as taxes, foreign-exchange losses and inconvenient trading hours.

MSCI's regular rebalancing, scheduled after the close on May 29, is also a flow variable. Some forecasts say up to 1.4 trillion won of passive funds could flow into Samsung Electronics and SK Hynix, considering an increase in South Korea's weighting and a reduction in the number of stocks compared with March. It remains necessary to check whether related expectations have already been largely reflected in share prices.

The Kosdaq could continue to benefit from policy momentum. The National Growth Fund is set to invest 7 trillion won this year, and market interest has grown as a 600 billion won tranche for retail investors was quickly sold out. The Kosdaq, which has a high weighting of growth industries such as pharmaceuticals and biotech and robotics, has reflected policy expectations relatively strongly.

By sector, the key is how much previously sidelined growth stocks and policy beneficiaries can follow while semiconductors take a breather. Last week, rotation buying emerged into areas such as pharmaceuticals and biotech, defence, and refining and chemicals while semiconductors and autos faced profit-taking pressure.

On the Kosdaq, pharmaceuticals and biotech stocks such as HLB, ABL Bio and Ligachem Bio were strong, along with secondary battery names such as EcoPro, EcoPro BM and Enchem.

Ultimately, this week's market appears to hinge more on "which sectors follow" than on another KOSPI push toward 8,000. If U.S. PCE inflation stabilises and the Bank of Korea stays within the market's expected range, rotation into Kosdaq growth stocks and non-semiconductor sectors could continue.

If interest rates and the currency jump again, or if volatility rises late in the session after the launch of single-stock leveraged ETFs, the indices could move back into a breather.

Lee Kyung-min (이경민), an analyst at Daishin Securities, said, "The KOSPI is currently in a typical earnings and macro-driven market," adding, "As the impact of upgraded earnings forecasts centred on semiconductors is strengthening the KOSPI's upside momentum, it is necessary to keep the upside open until earnings uncertainty comes in or earnings momentum passes its peak."